Are your finances healthy? Take test to find out

Are your finances healthy? Take test to find out.

Very few people will bother to keep tabs on how money flows out every month.

It's prudent to do a stock-take of what you have and owe

Tan Ooi BoonInvest Editor

Do you know how much you spend on your family every month? If your answer is "yes", you are probably wrong unless you run a tight ship in keeping every receipt and monthly bill.

This is perhaps the most difficult question for most working adults because very few people will bother to keep tabs on how money flows out every month.

If you use credit cards to pay for most things, the monthly statements are good starting points but these do not give the whole picture.

You have to look at other sources of outflow as well, such as your Giro payments for taxes, insurance policies, loans, rentals, membership and other fees, as well as telco and utility bills.

Then there are cash expenses, particularly for meals and other purchases at places that do not accept cards. You must also take note of the top-ups to your ez-link card and CashCard because transport and parking charges do add up. And don't forget the cash allowances you give your parents or children.

If you add all these up, you may be in for a shock when you realise that you need to spend so much every month.

To add to your woes, this list has not even included two significant expenses. One for emergencies such as visits to doctors and dentists or to stores and workshops when household items break down or need replacing. The other is for the family's enjoyment, such as birthday or anniversary gifts and holidays.

As all of us are spending more time at home now, it is prudent to do a stock-take of how much you have and how much you owe or need to spend.

Just like managing troops in a war, it is crucial to know what your "war budget" is so that you know where you can cut in case you need to divert more firepower elsewhere in times of need.

A silver lining in the current pandemic is that most households should see some form of savings in their monthly expenses for the past few months.

For those who have dutifully remained at home, you will be rewarded with big falls in transport-related charges as well as expenses for shopping, outings and dining out. Although grocery and utility bills are likely to have gone up, the overall increase should be much less than the savings from the other outgoings.

After all, a family meal at a restaurant prior to the circuit breaker could have set you back $100 to $200 but that same amount can now buy groceries for a week, unless you also live like a king at home.

If you find that you had been overspending before, it is a good time now to see how you can cut back on some non-essential expenses.

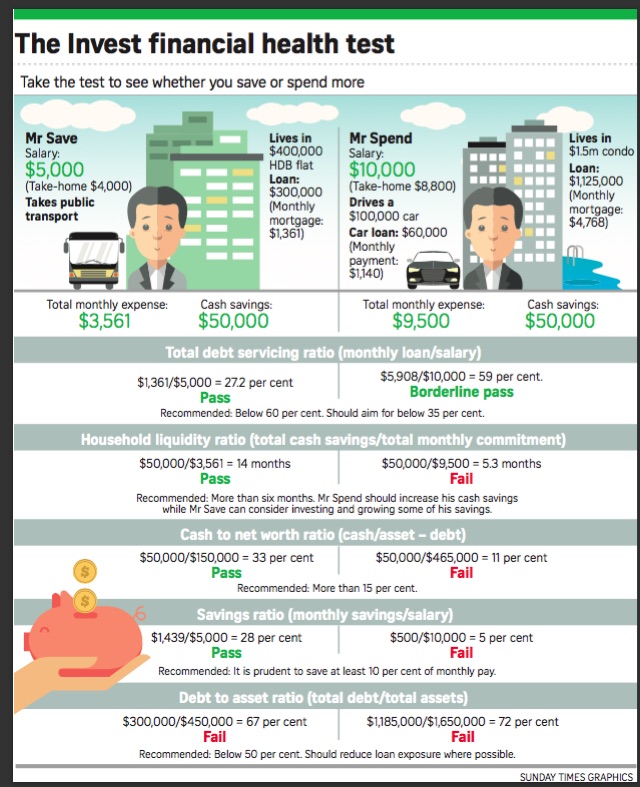

You can do a basic financial health check of your family expenses that Invest has put together with the help of Mr Alfred Chia, chief executive of financial advisory firm SingCapital. Just like health screenings, the five areas that you need to watch out for are:

1. TOTAL DEBT SERVICING RATIO (MONTHLY LOAN/SALARY)

This test is useful to gauge whether you are able to buy your dream home based on your income. If your intended home's monthly loan repayment plus your other debt obligations exceed 60 per cent of your income, it is a sign that you should look for a less expensive home.

2. HOUSEHOLD LIQUIDITY RATIO (TOTAL CASH/MONTHLY EXPENSE)

Calculate this by finding out your total monthly expenses and total cash savings. This will allow you to check whether you can ride out a crisis for at least six months in case you suddenly lose your fixed income. Gold jewellery and expensive watches usually don't count unless you are prepared to part with them at far lower prices.

3. CASH TO NET WORTH RATIO (CASH/ASSET - DEBT)

Just like managing troops in a war, it is crucial to know what your "war budget" is so that you know where you can cut in case you need to divert more firepower elsewhere in times of need.

This test determines whether you belong to the category of home owners who are asset-rich but cash-poor (below 15 per cent of the ratio). If you live in a multimillion-dollar home but have little cash savings, it may make more sense to downgrade to a smaller but still decent home so that you can have more to spend.

4. MONTHLY SAVINGS RATIO (MONTHLY SAVINGS/SALARY)

Those who watch what they spend will pass this test with flying colours. But if you fail to save even 10 per cent of your monthly income, you should probably impose a voluntary lockdown on your expenses once if not more times every week.

5. DEBT TO ASSET RATIO (DEBT/ASSET)

This test determines how strong your family's financial reserve is because it looks at the value of all assets, including property. The ideal ratio is below 50 per cent.

If you have investment properties, note whether they are still doing fine in a downturn.

People often assume that a man is deemed rich if he owns some real estate. But this ratio reveals the negative side if all the properties are supported by big loans. While the value of properties drops in a downturn, the loans for them will not.

SingCapital CEO Alfred Chia says that while there are good investment opportunities during the pandemic, the situation is still evolving and markets will be volatile.

Those who fail this test will face higher chances of foreclosure or even bankruptcy if things turn bad.

Many investors are very good at studying whether certain funds or companies are worth putting their money into. They forget that the best investment they will ever have is themselves.

So it pays to first check that you are financially healthy to weather any storm before you jump in to invest in other people's business.

BEING PRUDENT IS KEY TO SURVIVING CRISIS

Having a monthly salary of more than $10,000 seems like a pretty good deal but it does not automatically make you financially stable.

Indeed, even millionaires are not totally safe if they are heavily leveraged on risky investments because a sudden downturn could wipe out all their money.

"This may sound ironic but sometimes, rich people suffer even more in a crisis. This is because the more they have, the harder they fall. Ultimately, the safest bet is to be prudent with your financial health," says Mr Alfred Chia, chief executive of financial advisory company SingCapital.

He says many people like to plan their financial matters based on what they have seen or experienced in the past: "People who think like this will be painfully reminded of the common investment disclaimer that past performance should not be used as an indication for the future. Nobody could have predicted how hard Covid-19 is hitting all of us now."

This is why we should always be prudent with our money because a key function of financial planning is to ensure that we have sufficient means to tide us over a crisis.

Mr Chia notes that the pandemic is hurting freelancers and the self-employed the most. He cites two recent cases he has encountered.

CASE 1

A 40-something freelance fitness instructor who is a single parent of two teenage daughters. They live in a five-room HDB flat where each has her own room.

She has substantial Central Provident Fund (CPF) savings but little cash savings. As a result of the circuit breaker period, her income has dropped 90 per cent.

MR CHIA'S ADVICE

She qualifies for the Self-Employed Person Income Relief Scheme that will give her $1,000 a month for nine months. The girls can share one room and the family can rent out the other for supplementary income. Meanwhile, the mother can tap government grants to upgrade her skills.

When she resumes work, she will have to focus more on saving for the children's education and her retirement. She must continue to make voluntary contributions to her CPF account so that she has more to spend later on.

CASE 2

A couple in their 30s. The man is a private-hire car driver while his wife is a freelance tour guide.

His income has dropped more than 70 per cent as more people are now working from home. His wife is in a worse situation - she has no income as no one is going overseas for holidays now.

They have chalked up credit card debt of $12,000 due to overspending in the previous year. Both have little CPF savings except for funds in their Medisave accounts. They have an HDB loan that they repay with cash.

MR CHIA'S ADVICE

The couple would also qualify for the Self-Employed Person Income Relief Scheme of $1,000 a month for nine months. As their income has dropped more than 25 per cent, they can apply to convert their credit card debt to a term loan. By doing so, they will be able to reduce the card interest of 26 per cent to 8 per cent.

Like the earlier case, the couple should try to sign up for relevant government-supported courses to upgrade themselves. More importantly, when things return to normal, they should never neglect making voluntary CPF contributions to their accounts to build up their CPF savings.

Not all of Mr Chia's clients have been badly hit by the crisis. He says those who are professionals are relatively unscathed for now because they have been getting their usual salaries.

Indeed, those who have been prudent in their savings have approached him and asked whether it is a good time to jump into the market as most stocks have dropped significantly in the past few months.

Mr Chia warns these folk to tread very carefully because while many countries have started to reopen their economies, the world is still pretty much in a lockdown mode and recovery is likely to take a longer time.

"We agree that there are good investment opportunities. However, the situation is still evolving and markets will continue to be volatile. Covid-19 is one of those black swan events that will surprise many people," he adds.

Even if you are prepared to take the plunge, you should manage the risk by staggering your investments in the market in two or three tranches, and not everything in one go.

More importantly, avoid investing if you do not have the time and expertise to monitor the market.

"Look for a trusted adviser to guide you," Mr Chia says.

This is why it is prudent to first do a financial health check to make sure you have enough spare cash before you even think of investing.

And it is certainly foolish to invest money that you do not own, such as taking a loan from credit card firms just so you can try to make some money.

Doing so is very risky even in good times, more so now in this market when things can still turn very bad and make you run into huge debts.

The main purpose of investing is to ensure that you have sufficient means to have a good retirement. So if you barely pass the financial test, you will do better to leave your funds in your CPF account, which still earn a decent return even in these trying times.

Tan Ooi Boon

contact

SENIOR MARKETING DIRECTOR

CEA LICENSE: R027727H